Python:传统ARIMA及SARIMAX实现

发布于2019-08-07 11:40 阅读(5573) 评论(0) 点赞(3) 收藏(1)

传统ARIMA步骤:

加载数据:模型建立的第一步当然是加载数据集。

预处理:取决于数据集,预处理的步骤将被定义。这将包括创建时间戳、转换日期/时间列的dType、制作系列单变量等。

使系列平稳:为了满足假设,有必要使系列平稳。这将包括检查序列的平稳性和执行所需的变换。

确定值:为了使序列平稳,将执行差值操作的次数作为d值

创建ACF和PACF图:这是ARIMA实施中最重要的一步。ACF PACF图用于确定我们的ARIMA模型的输入参数。

确定p和q值:从前一步的图中读取p和q的值

拟合ARIMA模型:使用处理后的数据和我们先前步骤计算的参数值,拟合ARIMA模型

预测集上的预测值:预测未来价值

计算MSE或者RMSE:为了检查模型的性能,使用验证集上的预测和实际值检查MSE或者RMSE值

在实现的过程使用SARIMAX实现,这是一个包含季节趋势因素的ARIMA模型。

下面直接上代码:

data:直接采用 facebook 的prophet时序算法中examples的数据,可以在git上下载。

begin:

# Load data

df = pd.read_csv('data/example_air_passengers.csv')

df.ds = pd.to_datetime(df.ds)

df.index = df.ds

df.drop(['ds'], axis=1, inplace=True) y

ds

1949-01-01 112

1949-02-01 118

1949-03-01 132

1949-04-01 129

1949-05-01 121

# Resampling

df_month = df.resample('M').mean()

print(df_month.head())

y

ds

1949-01-31 112

1949-02-28 118

1949-03-31 132

1949-04-30 129

1949-05-31 121# 拆分预测集及验证集

df_month_test = df_month[-5:]

print(df_month_test.tail())

print('df_month_test', len(df_month_test))

df_month = df_month[:-5]

print('df_month', len(df_month))# PLOTS

fig = plt.figure(figsize=[15, 7])

plt.suptitle('sales, mean', fontsize=22)

plt.plot(df_month.y, '-', label='By Months')

plt.legend()

# plt.tight_layout()

plt.show()

# 看趋势

plt.figure(figsize=[15, 7])

sm.tsa.seasonal_decompose(df_month.y).plot()

print("air_passengers test: p={}".format( adfuller(df_month.y)[1]))

# air_passengers test: p=0.996129346920727

# Box-Cox Transformations ts序列转换

df_month['y_box'], lmbda = stats.boxcox(df_month.y)

print("air_passengers test: p={}".format(adfuller(df_month.y_box)[1]))

# air_passengers test: p=0.7011194980409873下一步观察季节差分及趋势差分,找出m及d。

# Seasonal differentiation

# 季节性差分确定sax中m参数

df_month['y_box_diff'] = df_month['y_box'] - df_month['y_box'].shift(12)

# 做个例子

最后得到的pvalue test diff13: p=0.000418 证明序列是稳定的。

下面进行模型选择及预测输出指标:

# SARIMAX参数说明

'''

趋势参数:(与ARIMA模型相同)

p:趋势自回归阶数。

d:趋势差分阶数。

q:趋势移动平均阶数。

季节性参数:

P:季节性自回归阶数。

D:季节性差分阶数。

Q:季节性移动平均阶数。

m:单个季节期间的时间步数。

'''# Initial approximation of parameters

Qs = range(0, 3)

qs = range(0, 3)

Ps = range(0, 3)

ps = range(0, 3)

D = 1

d = 1

parameters = product(ps, qs, Ps, Qs)

parameters_list = list(parameters)

# list参数列表

print('parameters_list:{}'.format(parameters_list))

print(len(parameters_list))

results = []

best_aic = float("inf")

for parameters in parameters_list:

try:

# SARIMAX 训练的时候用到转换之后的ts

model = sm.tsa.statespace.SARIMAX(df_month.y_box, order=(parameters[0], d, parameters[1]),

seasonal_order=(parameters[2], D, parameters[3], 12)).fit(disp=-1)

except ValueError:

print('wrong parameters:', parameters)

continue

aic = model.aic

if aic < best_aic:

best_model = model

best_aic = aic

best_param = parameters

results.append([parameters, model.aic])

result_table = pd.DataFrame(results)

result_table.columns = ['parameters', 'aic']

print(result_table.sort_values(by='aic', ascending=True).head())

print(best_model.summary())

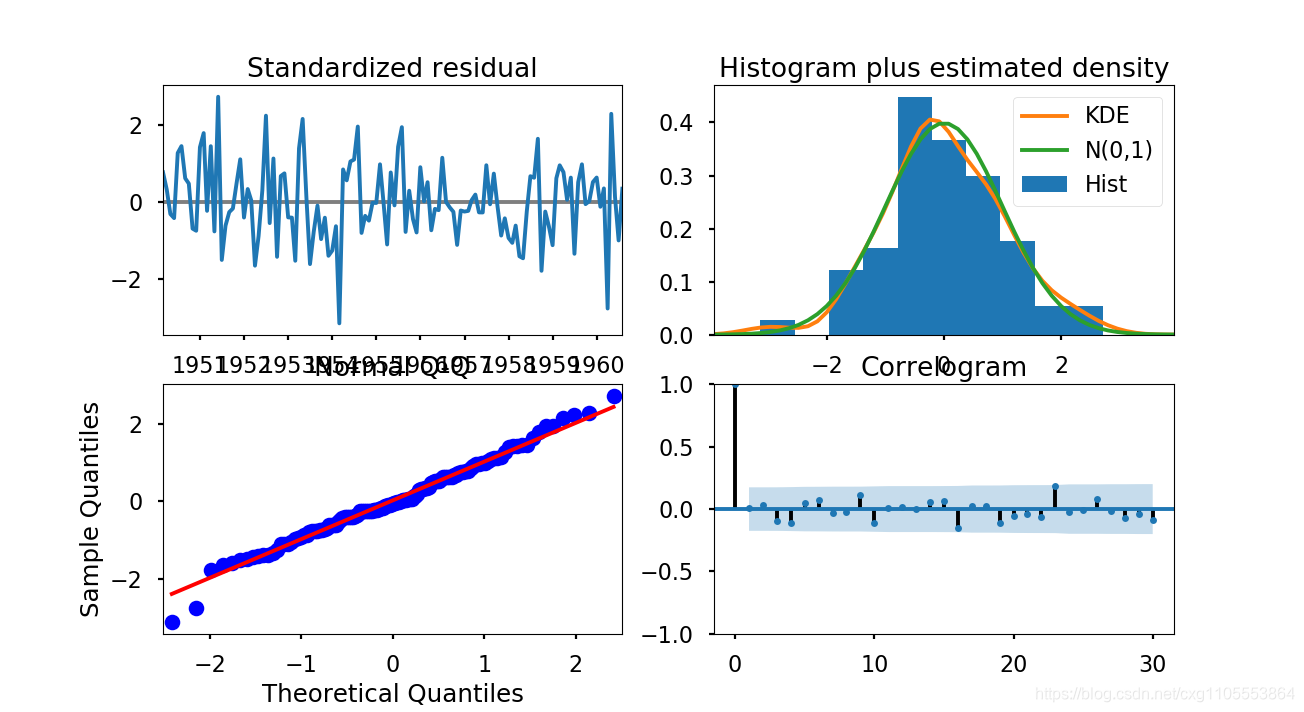

# Model: SARIMAX(0, 1, 1)x(1, 1, 2, 12) 得到 best_model 同时可以观察acf(resid)

sm.graphics.tsa.plot_acf(best_model.resid[13:].values.squeeze(), lags=48, ax=ax)

# 下图是对残差进行的检验。可以确认服从正太分布,且不存在滞后效应。

best_model.plot_diagnostics(lags=30, figsize=(16, 12))

验证结束之后最后对测试集预测并输出指标mse及rmse

df_month2 = df_month_test[['y']]

# best_model.predict() 设定开始结束时间

# invboxcox函数用于还愿boxcox序列

df_month2['forecast'] = invboxcox(best_model.forecast(steps=5), lmbda)

plt.figure(figsize=(15,7))

df_month2.y.plot()

df_month2.forecast.plot(color='r', ls='--', label='Predicted Sales')

plt.show()

# 获取mse

print('mean_squared_error: {}'.format(mean_squared_error(df_month2.y, df_month2.forecast)))

最后结果:#mean_squared_error: 90.93184037574731

结尾:

TS模块后续陆续更新auto_arima及lstm相应的概述及代码实现。

所属网站分类: 技术文章 > 博客

作者:gg

链接:https://www.pythonheidong.com/blog/article/10441/4dc7f8e82bfcb62462fc/

来源:python黑洞网

任何形式的转载都请注明出处,如有侵权 一经发现 必将追究其法律责任

昵称:

评论内容:(最多支持255个字符)

---无人问津也好,技不如人也罢,你都要试着安静下来,去做自己该做的事,而不是让内心的烦躁、焦虑,坏掉你本来就不多的热情和定力