使用SVR(支持向量回归机)的RBF(高斯核函数)拟合预测股票

发布于2019-08-22 17:00 阅读(3877) 评论(0) 点赞(28) 收藏(4)

目标:

根据2019-01-01 至 2019-07-30 , 沪市指数的收盘价, 使用SVR, 回归预测 2019-07-31( 或者2019-08-01)的收盘价

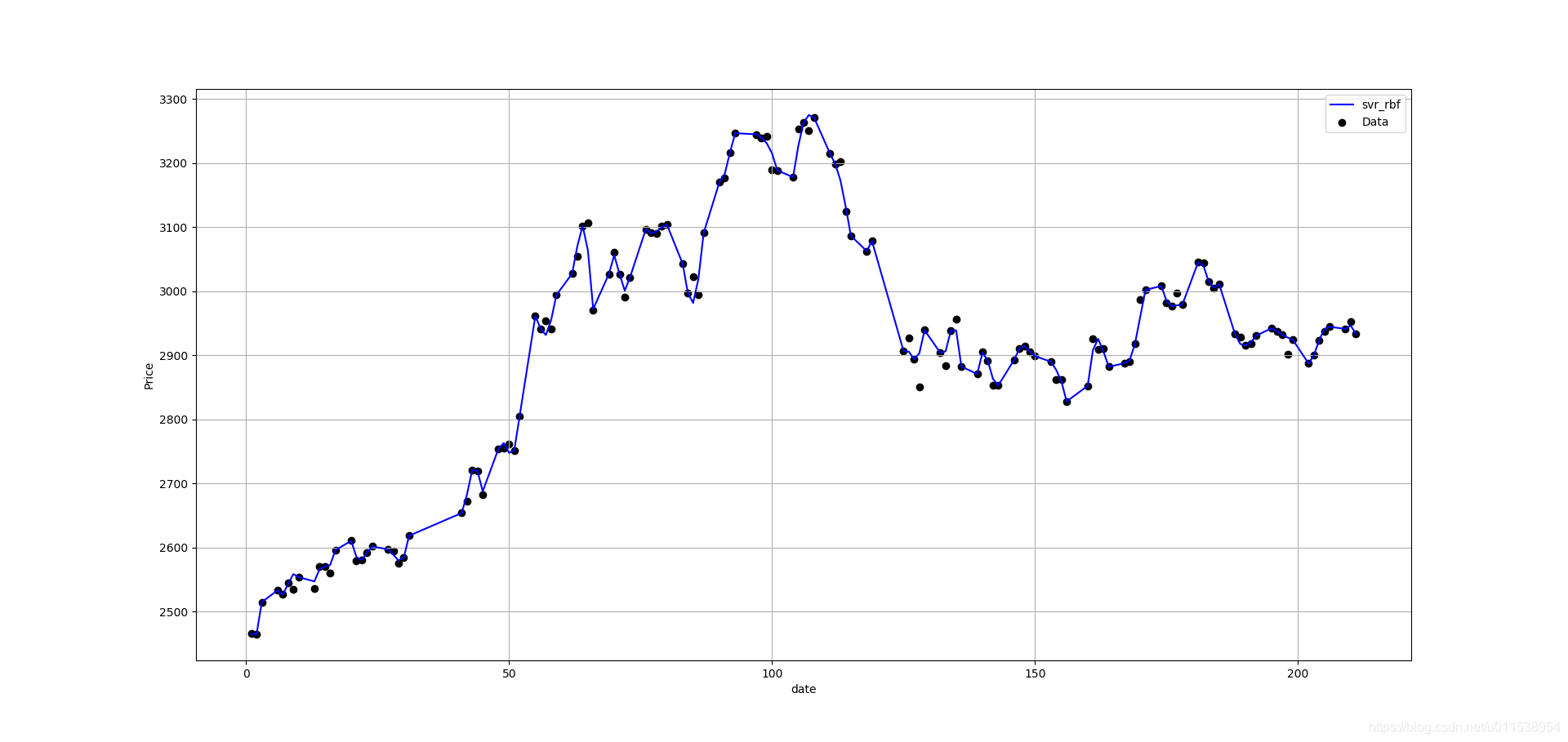

拟合结果:

[LibSVM]..........................*...........*

optimization finished, #iter = 10450

obj = -1700429.608042, rho = -2906.668575

nSV = 141, nBSV = 52

SVR(C=1000.0, cache_size=1000, coef0=0.0, degree=3, epsilon=0.1, gamma=0.1,

kernel='rbf', max_iter=-1, shrinking=True, tol=0.001, verbose=True)

2933.009977517439

拟合效果

实际K线图

代码

- import os

- import numpy as np

- import pandas as pd

- from scipy import stats

- import matplotlib.pyplot as plt

- from datetime import datetime as dt

- from sklearn import preprocessing

- from sklearn.svm import SVC, SVR

- import plotly.offline as of

- import plotly.graph_objs as go

- import tushare as ts

-

-

- # pip install ciso8601

- # pip install stockai

- def get_stock_data(stock_num, start):

- """

- 下载数据

- 股票数据的特征

- date:日期

- open:开盘价

- high:最高价

- close:收盘价

- low:最低价

- volume:成交量

- price_change:价格变动

- p_change:涨跌幅

- ma5:5日均价

- ma10:10日均价

- ma20:20日均价

- v_ma5:5日均量

- v_ma10:10日均量

- v_ma20:20日均量

- :param stock_num:

- :return:df

- """

- df = ts.get_hist_data(stock_num, start=start, ktype='D')

- return df

-

-

- def draw_kchart(df, filename):

- """

- 画k线图

- """

- Min_date = df.index.min()

- Max_date = df.index.max()

- print("First date is", Min_date)

- print("Last date is", Max_date)

- interval_date = dt.strptime(Max_date, "%Y-%m-%d") - dt.strptime(Min_date, "%Y-%m-%d")

- print(interval_date)

- trace = go.Ohlc(x=df.index, open=df['open'], high=df['high'], low=df['low'], close=df['close'])

- data = [trace]

- of.plot(data, filename=filename)

-

-

- def stock_etl(df):

- df.dropna(axis=0, inplace=True)

- # print(df.isna().sum())

- df.sort_values(by=['date'], inplace=True, ascending=True)

- return df

-

-

- def get_data(df):

- data = df.copy()

- # 年,月,天

- # data['date'] = data.index.str.split('-').str[2]

- # data['date'] = data.index.str.replace('-','')

- # print(data.index.tolist())

- data['date'] = [(dt.strptime(x, '%Y-%m-%d') - dt.strptime('2019-01-01', '%Y-%m-%d')).days for x in data.index.tolist()]

- data['date'] = pd.to_numeric(data['date'])

- return [data['date'].tolist(), data['close'].tolist()]

-

-

- def predict_prices(dates, prices, x):

- dates = np.reshape(dates, (len(dates), 1))

- x = np.reshape(x, (len(x), 1))

-

- svr_lin = SVR(kernel='linear', C=1e3,gamma=0.1, verbose=True, cache_size=1000)

- svr_poly = SVR(kernel='poly', C=1e3, degree=2, gamma=0.1, verbose=True, cache_size=1000)

- svr_rbf = SVR(kernel='rbf', C=1e3, gamma=0.1, verbose=True, cache_size=1000)

-

- plt.scatter(dates, prices, c='k', label='Data')

- # 训练

- # svr_lin.fit(dates, prices)

- # print(svr_lin)

- # print(svr_lin.predict(x)[0])

- # plt.plot(dates, svr_lin.predict(dates), c='g', label='svr_lin')

-

- # svr_poly.fit(dates, prices)

- # print(svr_poly)

- # print(svr_poly.predict(x)[0])

- # plt.plot(dates, svr_lin.predict(dates), c='g', label='svr_lin')

-

- svr_rbf.fit(dates, prices)

- print(svr_rbf)

- print(svr_rbf.predict(x)[0])

- plt.plot(dates, svr_rbf.predict(dates), c='b', label='svr_rbf')

-

- plt.xlabel('date')

- plt.ylabel('Price')

- plt.grid(True)

- plt.legend()

- plt.show()

- # return svr_lin.predict(x)[0], svr_poly.predict(x)[0], svr_rbf.predict(x)[0]

-

-

- if __name__ == "__main__":

- """

- 预测股价和时间之间的关系

- """

- # sh 获取上证指数k线数据

- # sz 获取深圳成指k线数据

- # cyb 获取创业板指数k线数据

- df = get_stock_data('sh', '2019-01-01')

- # + 张家港行

- # df = get_stock_data('002839', '2019-01-01')

- df = stock_etl(df)

-

- curPath = os.path.abspath(os.path.dirname(__file__))

- draw_kchart(df, curPath + '/simple_ohlc.html')

-

- dates, prices = get_data(df)

- print(dates)

- print(prices)

- # print(predict_prices(dates, prices, [31]))

- # print(predict_prices(dates, prices, ['20190731']))

- a = dt.strptime('2019-07-31', '%Y-%m-%d')

- b = dt.strptime('2019-01-01', '%Y-%m-%d')

- c = (a - b).days

- predict_prices(dates, prices, [c])

遇到问题: 使用多项式核函数, 60%的CPU跑了4个小时没有拟合出来.

使用线性核函数, 跑了40分钟才拟合出来结果.

使用高斯核函数,1分钟就拟合出结果了

源码:

https://github.com/clark99/learnMachinelearning/blob/master/sklearn/demo/svm/

所属网站分类: 技术文章 > 博客

作者:085iitirtu

链接:https://www.pythonheidong.com/blog/article/53122/fd4b771a0d783960b142/

来源:python黑洞网

任何形式的转载都请注明出处,如有侵权 一经发现 必将追究其法律责任

昵称:

评论内容:(最多支持255个字符)

---无人问津也好,技不如人也罢,你都要试着安静下来,去做自己该做的事,而不是让内心的烦躁、焦虑,坏掉你本来就不多的热情和定力